Quality Improvement Plan

Head Start/Early Head Start

Table of Contents

| Introduction |

| Corrective Action Goal #1: Compliance with HS 642© (1)(E)(iv)(V)(bb) |

| (Program Governance) |

| Corrective Action Goal #2: Compliance with 45 CFR 75.303(a) |

| (Ongoing Fiscal Capacity) |

| Corrective Action Goal #3: Compliance with 45 CFR 75.302 (b)(4) |

| (Financial management and financial management systems) |

Attachments:

- Board of Trustees Executive Committee and Finance Committee Meeting (October 21, 2019) Minutes

- Board of Trustees and Policy Council joint meeting (October 24, 2019) Minutes and Sign-in sheet

- Policy Council Votes via email

Introduction

| At the Burlington Community Action Partnership (BCAP), we are committed to continuous improvement of our programs/partnerships, services, process and procedures so that we may be effective at accomplishing our mission and vision. This Quality Improvement Plan (QIP) serves as both proof of this commitment and a guide for us to follow as we travel the path towards becoming an organization where quality improvement is inherent. The identified processes used are immediate and continuous is the ultimate goal in everything we do. The timeline for this process is as follow: |

| · In April 2019 BCAP received an on-site monitoring review of its Head Start and Early Head Start programs and as a result three “deficiencies” and three “areas of noncompliance” were noted as being in need of correction within 120 days. BCAP received the official monitoring report from the Office of Head Start on October 4, 2019. |

| · The BCAP administration and board representative engaged in a conference call with Office of Head Start (regional office) representatives on October 11, 2019 to review the monitoring report and ensured that the agency understood that a “Quality Improvement Plan” would need to be submitted within 30-days for “Regional Office” approval as to how the agency was going to correct the three “deficiencies” noted in the monitoring report of October 4, 2019. |

| · The administration sent out to the Board of Trustees and Policy Council members the full report via electronic mail (email) and postal mail on Tuesday October 15, 2019. |

| · On October 21st, 2019, administration held a joint meeting with the Executive Committee and Finance Committee of the BCAP Board of Trustees via conference call to discuss, review and accept the QIP to be submitted to the Office Head Start (regional office). |

| · The Board of Trustees and Policy held a joint meeting on Thursday, October 24, 2019 to discuss the “Draft Quality Improvement Plan”, which was sent to Board of Trustees and Policy Council members on Tuesday October 15, 2019. Both governing bodies approved the Quality Improvement Plan to be submitted to Office of Head Start. Only one member of the Policy Council was physically present at the meeting, and the approval from rest of the Policy Council members was obtained via email. |

| The administration will need to have all deficiencies and areas of noncompliance be corrected within 120-days, i.e., after 72 hours of receiving the monitoring report. Hence, submission of the QIP is due on November 10, 2019. The correction due date is Feb. 7, 2020. |

| The monitoring report indicated that in order for BCAP to be considered for continued HS/EHS funding the areas in HS/EHS will need to come into compliance with the following: |

| Citation: Title governing members adopt practices that ensure active, independent and informed governance of the Head Start agency (642 (c) (1) (E) (ii). The governing body members use data (both program data and external information) to oversee the provision of quality services for children and families and to ensure progress toward school readiness (1301.2(b) (2). |

| · The governing body members did not oversee the agency’s progress in carrying out programmatic provisions of the agency’s grant application (642(c) (I) (E) (IV) (V) (bb) |

| Citation: The grantee analyzes fiscal needs when selecting a fiscal officer (1302.91 (c). The grantee identifies assesses, and addresses risk such as natural disasters, child injury, and electronic theft, including insurance coverage, bonding, systems improvement and risk reduction measures (1303.52(b). |

| · The grantee did not implement staffing internal controls that support the program’s financial management systems (75.303(a) (b) and (e) |

| · The grantee did not effectively manage personnel compensation and fringe benefits. 653(a); 75.302(b)(4); 75.302(b)(3); 75.303(c); 75.303(d); 75.305(b)(1); 75.414; 75.430(I); 75.405(a); 75.441 |

| · The grantee did not maintain a complete inventory of all equipment purchased, in whole or in part with Head Start funds 75.320(d) (2). |

| Based on the results of the monitoring review BCAP and some prioritization of suggested strategies for furthering our journey to ensuring quality oversight of Head Start and Early Head Start funding to our agency, BCAP chose four main areas to focus our QIP on: |

| · Board Governance (Roles and Responsibilities) |

| · Policy Council Governance (Roles and Responsibilities) |

| · Fiscal Management (Policy and Procedures, Budget Execution, Allocation Plan, Procurement Plan) |

| · Human Resource Management (Personnel Policy, Employee Compensation) |

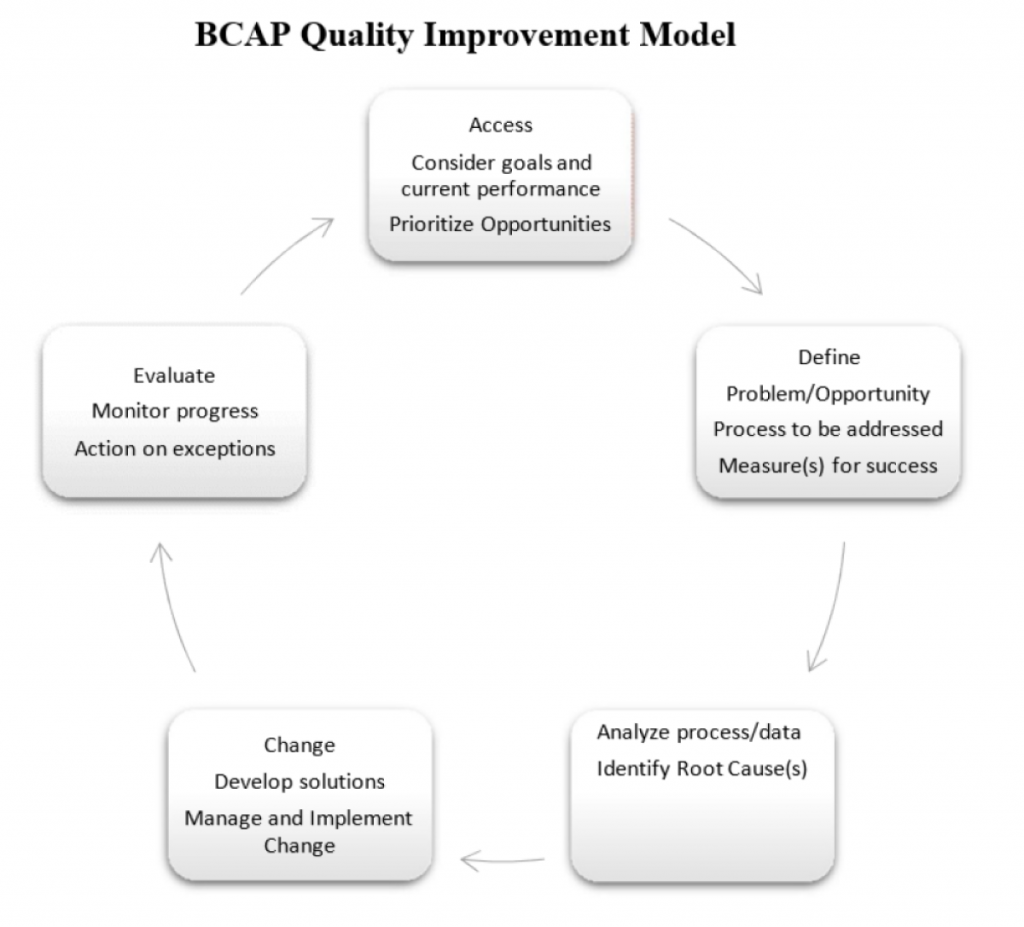

As an implementation plan has been developed for each goal area for the remainder of 2019 and into 2020. We will then evaluate progress on the goal areas, as well as the implementation of the QIP in general in preparation for ongoing continuous quality improvement plan (CQIP) for any updates or revisions in the 2020 plan.

A demonstrated quality improvement system has the potential to benefit not only the health of the organization but to the residents of the communities who depend on a quality “early learning” experience through our Head Start and Early Head Start program services. The credibility and efficiency of the Burlington Community Action Partnership organization to carry out the mandates of the grantee by implementing an effective QIP and sustained continuous process will support our agency in maintaining its legacy of offering Head Start and Early Head Start services.

Quality Improvement Leadership Team (QILT):

The BCAP QILT purpose is to create and maintain an internal system of quality improvement for the Head Start and Early Head Start programs that is clear, simple and quantifiable. BCAP will work with the Board of Trustees and Policy Council on forming a “Head Start QIP Committee”, who will monitor, review and recommend the progress of its implementation to the full governance of both bodies This will be an ad hoc committee that will meet with management on a monthly basis to get and update and review of the QIP progress. The QILT will report its QIP updates as required or mandated by the Office of Head Start (Regional II Office).

BCAP serves to create a system that:

- is realistic to implement,

- is acceptable to governance, management, and staff,

- is dynamic and allows for adjustment based on future needs,

- does not increase workload for staff,

- utilizes existing data and existing work processes wherever possible,

- provides a high benefit for its efforts,

- allows changes to improve programs and services based on measurement and processes,

- ultimately leads to increasingly effective management systems for accountability;

- contributes to a strong system of management

The quality improvement leadership team (QILT) is necessary to provide leadership and accountability to the task of bringing about a quality improvement plan process. The team will set direction; identify needs, resources, and priorities; facilitate the process; maintain momentum; and recognize results in the continuous

improvement effort. QILT will collect information about ongoing quality improvement efforts and assist the staff in the implementation of continuous quality improvement so that the benefits of the process reach all of its customers and stakeholders, including staff.

QILT members will include the Chief Executive Officer, Chief Fiscal Officer, Chief Operating Officer, Head Start/Early Head Start Director, Human Resource Director, Head Start Leadership Team members and identified stakeholders. QILT will work towards a continuous improvement system that delivers quality data and encourages improvement to the managing of the Head Start and Early Head Start programs. QILT will collect information about ongoing quality improvement efforts and assist the governance bodies and staff in the implementation of continuous quality improvement so that the benefits of the process reach all of its customers and stakeholders, including staff.

The Head Start QI Committee will include three members of the Board of Trustees, three members of the Policy Council and each member will be appointed by the Chairs of each governing body. The Committee will also include the Board Chairs, Chief Executive Officer, and staff as “ad hoc” committee members for guidance and support.

Corrective Action Goal #1

Corrective Action Goal #1: Compliance with HS 642© (1)(E)(iv)(V)(bb) |

||

| Program Governance: To improve the efficiency and implementation to ensure that the BCAP Board of Trustees and Policy Council maintain a formal structure of program governance to oversee the quality of services for children and families and to make decisions related to programs design and implementation. | ||

Objective 1 |

Objective 2 |

Objective 3 |

|

Board of Trustees will attend a mandatory training to review their governance responsibilities to ensure that members adopt practices that they adopt are active, independent, and informed governance of Head Start agency 642(c) (1) (E) (ii); 1301.2(b)(2); 642(c)(1)(E)(iv)(V)(bb) |

Policy Council members will attend a mandatory training to review their governance responsibilities to ensure that members adopt practices that are active, independent, and informed governance of Head Start Agency 642 (c)(2)(D)(i);1302.102(d) | Board of Trustees and Policy will review existing shared governance policies, such as Board of Trustee bylaws and Policy Council bylaws to ensure that they are aligned and that no conflict of governance responsibilities exist, such as hiring and termination of staff members within the Head Start programs. |

Expected Outcome(s) |

||

| The governance bodies of the Head Start and Early Head Start programs will be aware of their respective roles and responsibilities and ensure that they are properly implementing the Head Start Act (2007) and Head Start Performance Standards (2016) by following the law and standards as prescribed. | ||

Description of Deficiency |

||

|

The governing body members did not oversee the agency ‘s progress in carrying out programmatic provisions of the agency’s grant application. 642(c)(I)(E)(iv)(V)(bb)

Sec. 642 Powers and Functions of Head Start Agencies (c) Program Governance- Upon receiving designation as a Head Start agency, the agency shall establish and maintain a formal structure for program governance, for the oversight of quality services for Head Start children and families and for making decisions related to program design and implementation. Such structure shall include the following: ( I) GOVERNING BODY- (E) RESPONSIBILITIES- The governing body shall (iv) be responsible for other activities, including– (V) reviewing and approving all major policies of the agency, including–(bb) such agency’s progress in carrying out the programmatic and fiscal provisions in such agency’s grant application, including implementation of corrective actions. |

||

Corrective Action Goal #2

Corrective Action Goal #2: Compliance with 45 CFR 75.303(a) |

||

|

Ongoing Fiscal Capacity: BCAP will establish and maintain effective internal control over the Federal award that provides reasonable assurance that the non-Federal entity is managing the Federal award in compliance with Federal statutes, regulations, and the terms and conditions of the Federal award. Ensure these internal controls shall be in compliance with guidance in “Standards for Internal Control in the Federal Government,” issued by the Comptroller General of the United States or the “Internal Control Integrated Framework,” issued by the Committee of Sponsoring Organizations of the Treadway Commission (COSO). The root causes that resulted in the non-compliance findings were as follows: 1. Weak Internal Controls 2. Outdated Fiscal policies 3. Lack of staff training and skill set |

||

Objective 1 |

Objective 2 |

Objective 3 |

| Management will review and update BCAP’s Internal Control Policy that will ensure compliance with 75.303 and follow the COSO guidelines in internal controls. | Management will update/revise its Fiscal Policies and Procedures to ensure they fully address effective control and accountability or all funds in compliance with the terms and conditions of the grant award including compliance with the Uniform Guidance (45 CFR Part 75), Head Start Act of 2007 and HSPPS, to be submitted to the Board of Trustees and Policy Council for final approval and adoption. Such revisions/updates will address specifically such “deficiencies” including “areas of noncompliance” noted but not limited to: Internal Controls, Procurement, Cost Principles, Cost allocation, Budget execution, Indirect and Administrative Costs. | Management will ensure its fiscal staff receive fiscal training to strengthen their fiscal knowledge and ensure fiscal compliance. |

Expected Outcome(s) |

||

| The Burlington Community Action Partnership’s fiscal management system will provide for the adequate safeguarding and usage of all assets for authorized purposes only, by establishing and maintaining effective internal controls in accordance with Federal rules and regulations. | ||

Responsible Persons Abbreviations |

||

| CEO – Chief Executive Officer | ||

| COO – Chief Operating Officer | ||

| CFO – Chief Financial Officer | ||

| FT – Finance Team | ||

| FC – Finance Committee | ||

| BT – Board of Trustees | ||

| PC – Policy Council | ||

| HR DIR – Human Resources Director | ||

| BPC – Board Personnel Committee | ||

| HSD – Head Start Director | ||

| PCC – Personnel Committee | ||

| HSC – Head Start Committee | ||

Description of Deficiency

75.303 Internal controls. The non- Federal entity must: (a) Establish and maintain effective internal control over the Federal award that provides reasonable assurance that the non-Federal entity is managing the Federal award in compliance with Federal statutes, regulations, and the terms and conditions of the Federal award. These internal controls should be in compliance with guidance in “Standards for Internal Control in the Federal Government,” issued by the Comptroller General of the United States or the “Internal Control Integrated Framework,” issued by the Committee of Sponsoring Organizations of the Treadway Commission (COSO).

Corrective Action Goal #3

Corrective Action Goal #3: Compliance with 45 CFR 75.302 (b)(4)

BCAP will ensure its financial management system provides for the adequate safeguarding of all assets and must also ensure they are used solely for authorized purposes.

a. The financial management system of BCAP will:

- Provide for the effective control over, and accountability for, all funds, property, and others.

- Adequately safeguard all assets and assure that they are used solely for authorized purposes.

- Have records that identify adequately the source and application of funds for federally funded.

- Have records that must contain information pertaining to Federal awards, authorizations, obligations, unobligated balances, assets, expenditures, income, and interest and be supported by the source.

- Evaluate and monitor the non-Federal entity’s compliance with statutes, regulations, and the terms and conditions of Federal.

- Take prompt action when instances of noncompliance are identified including noncompliance identified in an audit.

b. BCAP will minimize the time elapsing between the transfer of funds from the United States Treasury or the pass-through entity and the disbursement by the non-Federal entity whether the payment is made by electronic funds transfer, or issuance or redemption of checks, warrants, or payment by other means. See also §75.302(b)(6). Except as noted elsewhere in this part, HHS awarding agencies must require recipients to use only OMB- approved standard governmentwide information collection requests to request.

c. Allowable activities by BCAP:

- Charges to Federal awards may include reasonable amounts for activities contributing and directly related to work under an agreement, such as delivering special lectures about specific aspects of the ongoing activity, writing reports and articles, developing and maintaining protocols (human, animals, etc.), managing substances/chemicals, managing and securing project-specific data, coordinating research subjects, participating in appropriate seminars, consulting with colleagues and graduate students, and attending meetings and

d. BCAP will have a system in place to identify, allocate and accurately report the administrative and programmatic portions of costs for all Federal and non-Federal

e. BCAP will ensure compliance with Davis Bacon Act. All the construction contracts in excess of $2,000 paid with Head Start funds will include a provision for compliance with the Davis-Bacon Act.

f. BCAP will seek prior approval from OHS if the transfer between the budget categories is needed that exceeds $250,000

g. BCAP will ensure compliance with CFR 75.405(a) and Procurement standards per 45 CFR Part 75.A cost is allocable to a particular Federal award or other cost objective if the goods or services involved are chargeable or assignable to that Federal award or cost objective in accordance with relative benefits received. This standard is met if the cost:

- Is incurred specifically for the Federal.

- Benefits both the Federal award and other work of the non-Federal entity and can be distributed in proportions that may be approximated using reasonable methods.

- It is necessary to the overall operation of the non-Federal entity and is assignable in part to the Federal award in accordance with the principles in this subpart.

- Costs resulting from non-Federal entity violations of, alleged violations of, or failure to comply with, Federal, state, tribal, local or foreign laws and regulations are unallowable, except when incurred as a result of compliance with specific provisions of the Federal award, or with the prior written approval of the HHS awarding.

h. BCAP will have a system in place to identify, allocate and accurately report the administrative and development portion of costs, both Federal and non-Federal, charged to Head Start.

i. BCAP will ensure compliance with Procurement standards per 45 CFR Part.

j. BCAP will ensure its property management is in accordance with 45 CFR 75.320 (d) (2)

k. BCAP will make sure that a physical inventory of equipment is done and its results are reconciled with its equipment records at least once every two

l. BCAP will ensure that lines of credit will never be charged against or be secured by any Head Start and Early Head Start assets. BCAP will never use any Head Start funds to secure its lines of credit. BCAP will ensure it will manage its cash flow

m. BCAP will seek prior approval from OHS if it will move funds from the Personal Services to OTPS which is beyond the allowable threshold of $250,000.

n. BCAP will now always ensure that compensation for personal services satisfies the standards of personnel expenses.

Objective 1 |

Objective 2 |

Objective 3 |

| BCAP will establish and maintain effective control over, and accountability for, all its funds, property, and other assets in accordance with 75.320. | BCAP will adequately safeguard all assets and assure that they are used solely for authorized purposes |

BCAP will set up a system for determining whether individual expenses are necessary, reasonable, allocable, and adequately documented. 75.302(b)(7); 75.328(a)(4)(5)(7); 75.328(b); 75.329(a)-(b); 75.403(a)- (g); 75.329(a)-(b); 75.332;75.327(h) |

Expected Outcome(s) |

||

| The Burlington Community Action Partnership’s fiscal management system ensures the adequate safeguarding of all assets and their usage for authorized purposes only. The Board of Trustees and Management will build and maintain a fiscal management system that supports the organization’s ongoing capacity to monitor and utilize federal funds as per the federal standards. | ||

Description of Deficiency |

||

| 75.302 Financial management and standards for financial management systems. (b)The financial management system of each non-Federal entity must provide for the following (see also§§75.361, 75.362,75.363, 75.364, and75.365): (4) Effective control over, and accountability for, all funds, property, and other assets. The non-Federal entity must adequately safeguard all assets and assure that they are used solely for authorized purposes. See §75.303. | ||

Section 1 - QIP Approval

Section 2 – QIP Governance Section

QIP Action 1 |

|

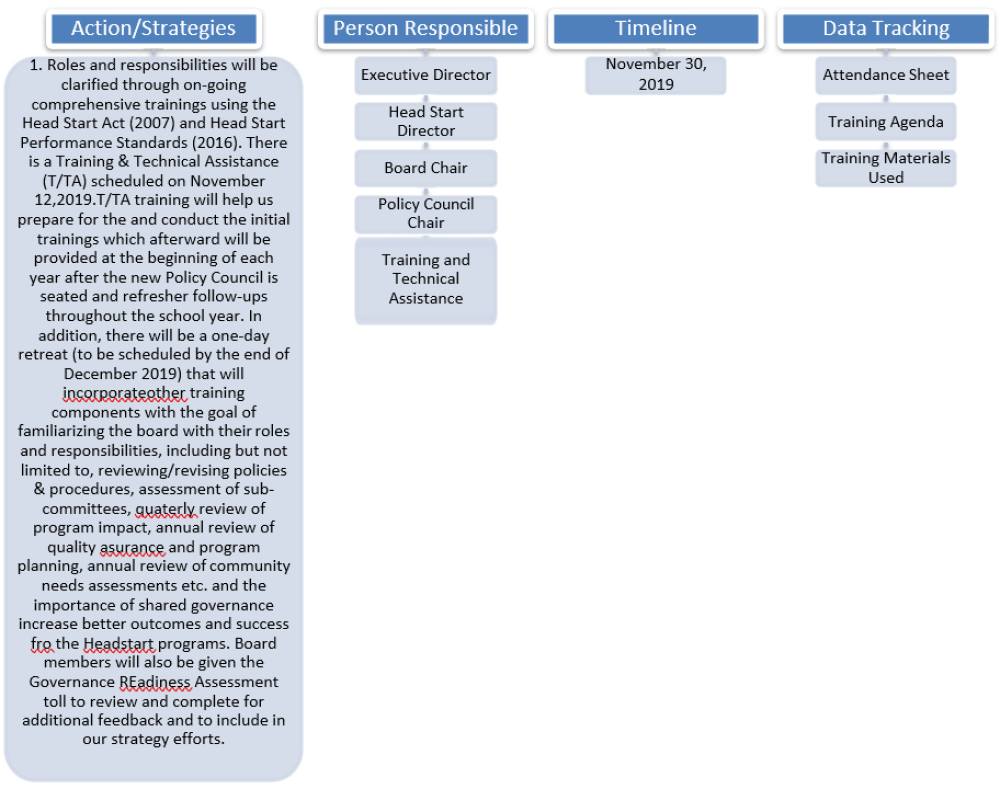

Roles and responsibilities will be clarified through on-going comprehensive trainings using the Head Start Act (2007) and Head Start Performance Standards (2016). There is a Training & Technical Assistance (T/TA) scheduled on November 12, 2019. T/TA Training will help us prepare for and conduct the initial trainings, which afterward, will be provided at the beginning of each year after the new Policy Council is seated. Refresher follow-ups throughout the year will also be conducted. In addition, there will be a one-day retreat (to be scheduled by the end of December 2019) that will incorporate other training components with the goal of familiarizing the Board with their roles and responsibilities, including but not limited to, reviewing/revising policies & procedures, assessment of sub-committees, a quarterly review of program impact, annual review of quality assurance and program planning, annual review of community needs assessments, etc., and the importance of shared governance. This will increase better outcomes and success for the Head Start programs. Board Members will also be given the Governance Readiness Assessment tool to review and complete for additional feedback and to include in our strategic efforts. |

QIP Action 2 |

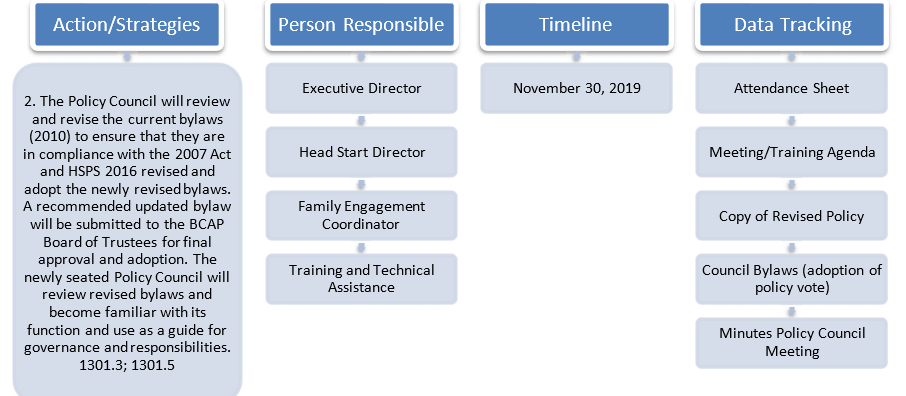

| By-Laws Request For Approval – Emails |

QIP Action 3 |

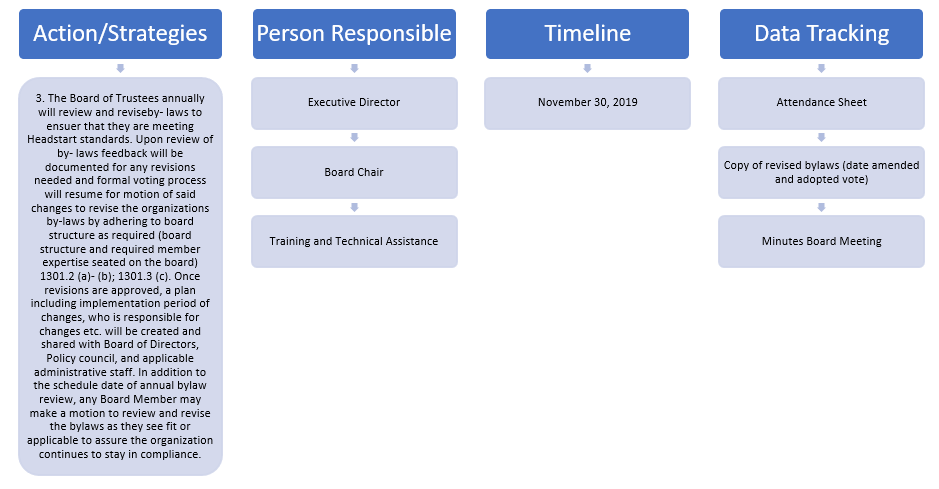

| Board of Trustees Monthly Meeting Minutes – September 17, 2019 |

QIP Action 4 |

|

The Board of Trustees will assign a Board representative to serve as a non-voting member to the Policy Council for the purpose of sharing Board decisions on matters that directly affect the policy and procedures (changes, revisions/updates). The Board of Trustees will share its minutes with the Policy Council to ensure that all actions are noted and whether they directly affect the Head Start and Early Head Start programs. Clarification will come from the appointed Board representative. 1302.102(a) Please click here to refer to Appendix I, Article VI, Section K |

QIP Action 5 |

|

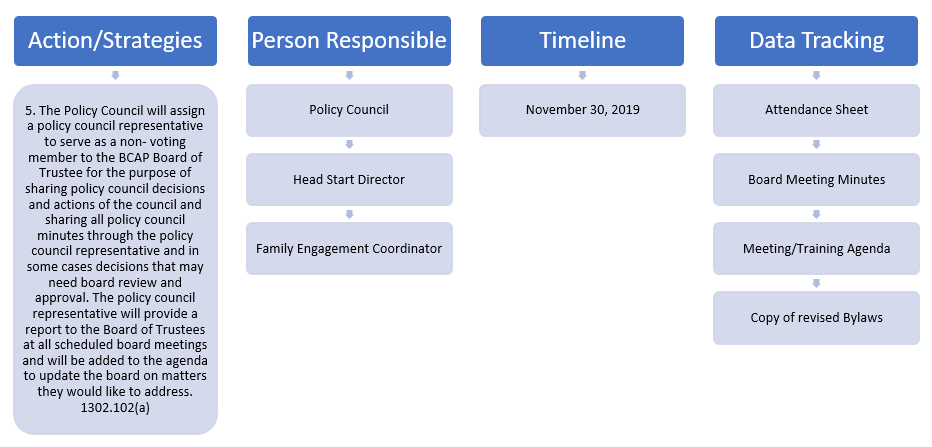

The Policy Council will assign a Policy Council representative to serve as a non-voting member to the BCAP Board of Trustees for the purpose of sharing Policy Council decisions and actions of the Council and sharing all Policy Council minutes through the Policy Council representative and, in some cases, decisions that need board review and approval. The Policy Council representative will provide a report to the Board of Trustees at all scheduled Board meetings and will be added to the agenda to update the Board on matters they would like to address. 1302.102(a) Please click here to refer to Appendix I, Article VI, Section L. |

QIP Action 6 |

|

The BCAP Board of Trustees and Policy will jointly draft and adopt an “internal dispute resolution”. This process will be followed by both the governing bodies to resolve, in the event that a potential or existing conflict occurs. 1301.6 |

QIP Action 7 |

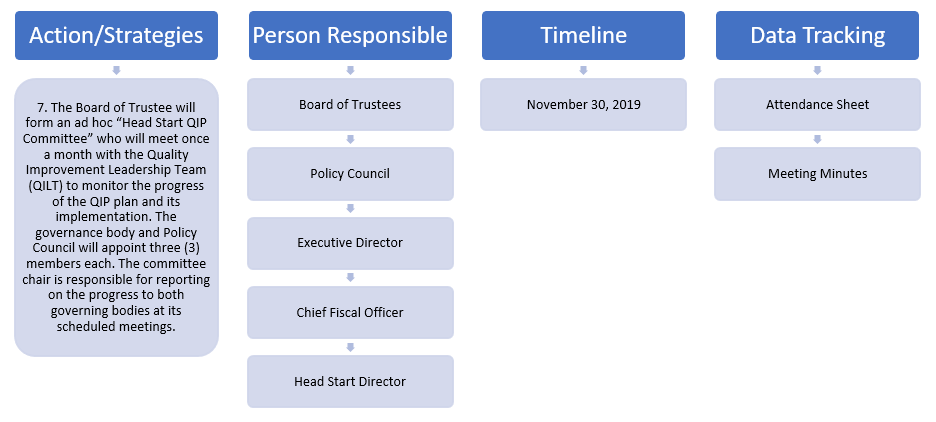

| The Board of Trustees will form an ad hoc “Head Start QIP Committee” who will meet once a month with the Quality Improvement Leadership Team (QILT) to monitor the progress of the QIP Plan and its implementation. The governance body and Policy Council will appoint three (3) members each. The committee chair is responsible for reporting on the progress to both governing bodies at is scheduled meetings. |

QIP Action 8 |

|

The Board of Trustees and Head Start Policy Council will attend trainings to review their governance responsibilities, Financial Management, and Fiduciary responsibilities to ensure that members adopt practices that adopt active, independent, and informed governance of the Head Start agency. If someone is unable to attend, materials and minutes from the meeting will be provided. There will also be “make-up” trainings made available quarterly for those who may not be able to attend.

Please refer to Action Item 1. Click here to see the Head Start and Early Head Start Governance Manual. |

QIP Action 9 |

|

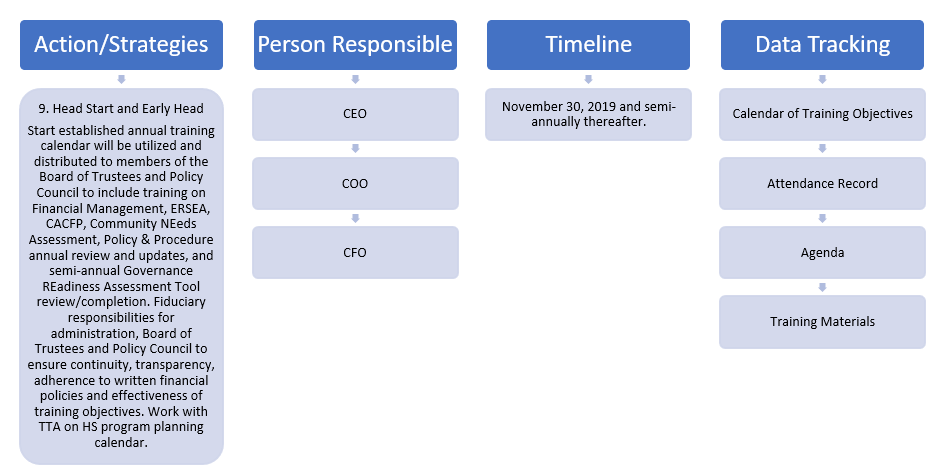

Head Start and Early Head Start established an annual training calendar that will be utilized and distributed to members of the Board of Trustees and Policy Council to include training on Financial Management, ERSEA, CACFP, Community Needs Assessment, Policies & Procedures annual review and updates, and semi-annual Governance Readiness Assessment Tool review/completion. Fiduciary responsibilities for Administration, Board of Trustees, and Policy Council to ensure continuity, transparency, adherence to written financial policies and effectiveness of training objectives. Work with T/TA on Head Start program planning calendar. |

Section 3 – QIP Fiscal Section

Corrective Action Goal #2 – Action 1 |

|

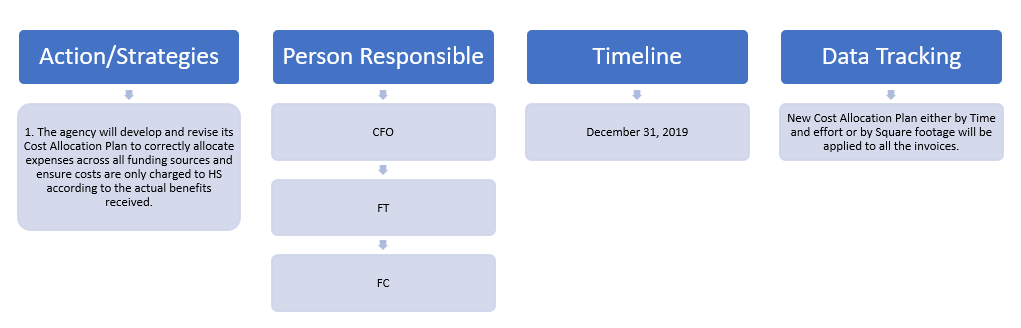

The Agency will develop and revise its Cost Allocation Plan to correctly allocate expenses across all funding sources and ensure costs are only charged to Head Start according to the actual benefits received. |

Corrective Action Goal #2 – Action 2 |

|

Update/Revise FP&Ps in Cost Allocation to ensure compliance with the Uniform Guidance. |

Corrective Action Goal #2 – Action 3 |

|

Establish cost methodology in allocating costs (consultants, contracted labor, and professional services, supplies, etc.). |

Corrective Action Goal #2 – Action 4 |

|

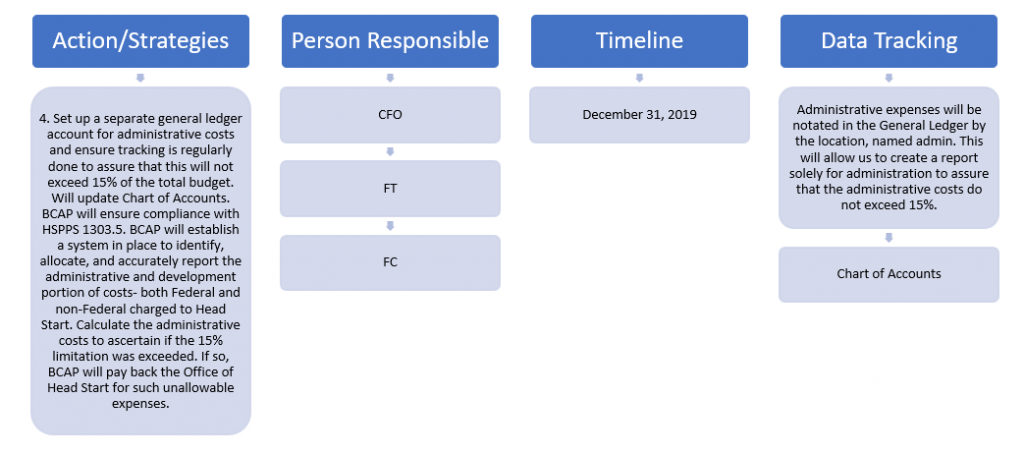

Set up a separate general ledger account for administrative costs and ensure tracking is regularly done to assure that this will not exceed 15% of the total budget. Will update Chart of Accounts. BCAP will ensure compliance with HSPPS 1303.5. BCAP will establish a system in place to identify, allocate, and accurately report the administrative and development portion of costs, both Federal and non-Federal, charged to Head Start. Calculate the administrative costs to ascertain if the 15% limitation was exceeded. If so, BCAP will pay back the Office of Head Start for such unallowable expenses. Administrative costs for the periods in question did not exceed 15% of total Head Start / Early Head Start Expense. Fiscal Year 2017 to 2019 are 13.2%, 9.0% and 11.3% respectively. Refer to the following attachments for each year in the following order HS Admin Cost Calculation, Head Start FY Reconciliation, Schedule of M-G Expense (per audit) and Head Start General Ledger. Appendix V-Z to V-AK. Appendix V-Z – HS Admin Cost Calculation FY2017 Appendix V-AA – Headstart FY 2017 Reconciliation Appendix V-AB – Schedule of M-G Expense – 2017 Appendix V-AC – Headstart General Ledger FY 17 Appendix V-AD – HS Admin Cost Calculation FY2018 Appendix V-AE – Headstart FY 2018 Reconciliation Appendix V-AF – Schedule of M-G Expense – 2018 Appendix V-AG – Headstart General Ledger FY 18 Appendix V-AH – HS Admin Cost Calculation FY2019 Appendix V-AI Headstart FY 2019 Reconciliation Appendix V-AK – Headstart General Ledger FY 19 Fiscal year 2020 audit is currently in progress, so general ledger support and administrative cost calculation will not be available until audit is finalized. |

Corrective Action Goal #2 – Action 5 |

|

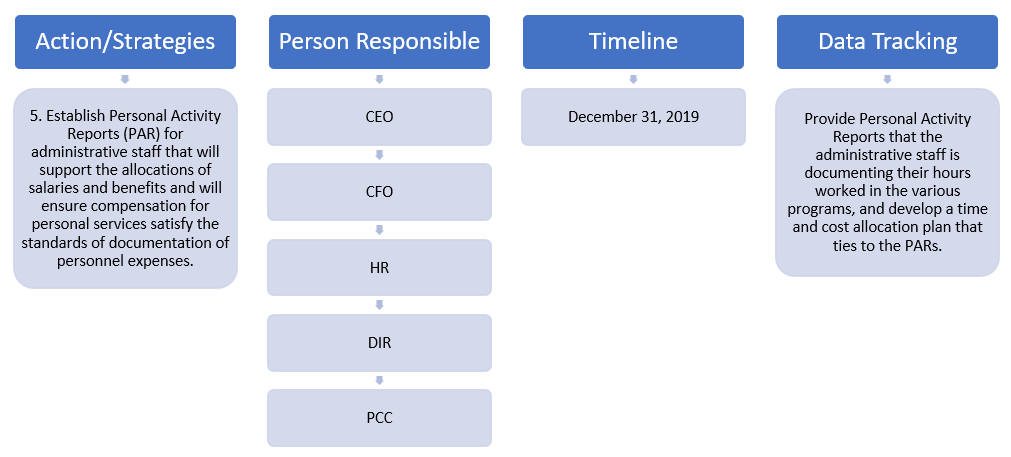

Establish Personal Activity Reports (PAR) for administrative staff that will support the allocations of salaries and benefits and will ensure compensation for personal services satisfy the standards of documentation of personnel expenses. The percentage allocated of staff time to a grant program is based on time and effort analysis and historical efforts used to budget allocated staffing to each grant program. Per Accounting Policies and Procedures, Section 15. Cost Allocation, as of the inception date of the policies and procedures, 2/25/2020, payroll expense for employees assigned to more than one program are allocated based on percentage reported on after-the-fact determination reports, Personnel Activity Report, or “PARs”. This report is reconciled semi-annually to charges in the general ledger and are restated to reflect actual time worked by grant based on the Personnel Activity Report. In prior fiscal years the PARs were also created by employees to track employee activity, but some percentages were based on budgeted allocation percentages derived from time studies performed. Employee and supervisor signatures are requested at time of completion on the PARs forms, although not all forms submitted for review are signed copies. Due to the changes in finance department staffing not all signed copies were able to be located, but we are working to become 100% compliant going forward.

Appendix V-G – Personnel Activity Report – M. Gill 2017-18 Appendix V-H – Personnel Activity Report – M. Gill – 2018-19 Appendix V-I – Personnel Activity Report – M. Gill – 2019-20

PARs Fiscal Year 2019 Executive Director, Human Resource Director and Accountant: Appendix V-K Personnel Activity Report – K. Edwards 2018-19 Appendix V-L – Personnel Activity Report – A. Sharer 2018-19

Documentation for FY2019 Summary of Salaries Executive Director, Human Resource Director and Accountant: |

Corrective Action Goal #2 – Action 6 |

|

Appendix V – Summary of Head Start Invoices – summarizes the reallocation of expenditures identified during the onsite monitoring. Appendix V-A – CohnReznick Invoice for $80,000 corrected allocation resulted in a decrease of expense to the Headstart Programs of $43,200. Appendix V-B – Staples Check Request and Invoices – Supports the amount paid of $19,396 to Staples identified in the Monitoring Response. Note that the actual amount paid to Staples for the purchase in question, PO 55283, was actually $18,060.45. Appendix V-C – Summary of Head Start Invoices – Staples Detail – summarizes the total of PO 55283 by invoice number, lists computers by user/location, and allocation of expense. Locations of each computer received in March of 2018 as of August 2020 determined 9 computers, not 6, were assigned to staff that were not direct Head Start staff. The original allocation of $18,060.45 was decreased to $14,468.01 to account for the actual use of these 9 computers. Appendix V-D – 1SEO Technologies Invoices identified in the monitoring report were reviewed and attached for reference. All invoices for the period were also reviewed to determine if correct allocations were utilized. The invoice 61838 for $10,020 allocation to headstart program was revised to $4,029.60 and invoice for $8,212.50 allocation to headstart was revised to $5,037.02. Additional invoices during this period also were incorrectly allocated resulting in invoice #62649 increase of $324.64 and invoice #62090 increase of $770.14. The adjusted total was a decrease of $8,071.10. Appendix V-E – Selective Insurance invoices are provided for your reference. A review of accounting records determined that the Selective Insurance invoices had not been properly allocated. These invoices have been correct to reflect the proper expenditures by program. Selective insurance invoices review resulted in an increase of $2,052.00, $1,055.81 and $2,110.99 for a total increase of expense of $5,218,80. Appendix V-F – Posted General Ledger Transactions Invoice Correction – shows the entries recorded in the general ledger to update expenditures Summary |

Corrective Action Goal #2 – Action 7 |

|

Ongoing monitoring of fiscal compliance with Head Start Act of Uniform Guidance. |

Corrective Action Goal #2 – Action 8 |

|

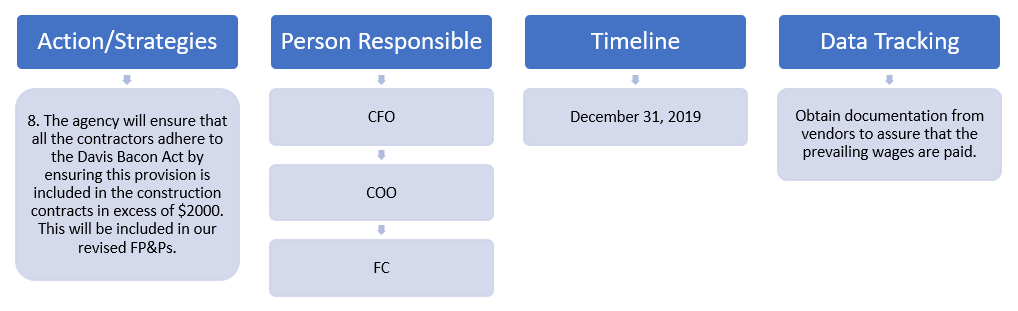

The agency will ensure that all the contractors adhere to the Davis Bacon Act by ensuring this provision is included in the construction contracts in excess of $2000. This will be included in our revised FP&Ps. Please click here refer to Appendix II and click here for V-R. |

Corrective Action Goal #2 – Action 9 |

|

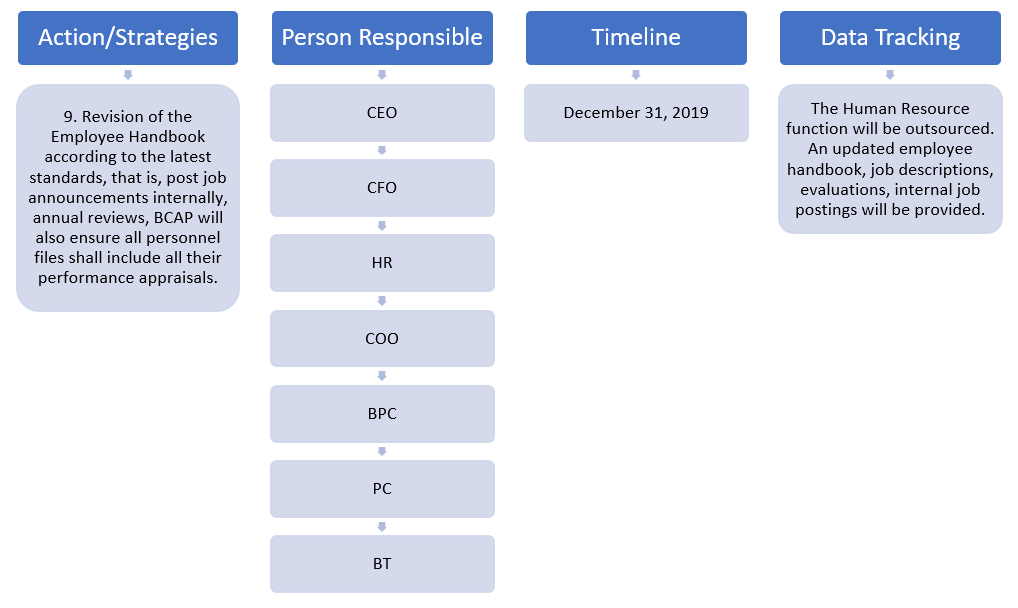

The Chief Operating Officer, COO, Manvir Gill was promoted to positions he was not hired for initially. It was determined within 2 weeks of his hire that he was needed to perform duties beyond, the accountant position he was hired for. (Appendix V-N – Chief Operating Officer Job Responsibilities) He met the qualifications in education and personal drive to accomplish the tasks and was performing the duties of each position title prior to being officially assigned the position title. His initial duties quickly expanded over the 11 month period of time resulting in the title changes and acting roles and increases in pay justified by management to awarded retroactively based on his daily performance and accomplishments. The role of Controller was assigned briefly due to a staffing vacancy. BCCAP has subsequently reviewed procedures of posting positions both internally and externally prior to award of positions and will adhere to the revised procedure going forward as stated in Employee Handbook. Likewise, annual evaluations will be performed for all staff and placed in their personnel files. The following attachments support statements above have been implemented: Per the analysis completed it was determined that COO was not allocated to Head Start at 63% to 96% as stated in the Program Performance Summary Report. COO was allocated to Head Start at 37% during Fiscal Year 2018, 45% Fiscal Year 2019, and 40% Head Start and 5% Early Head Start Fiscal Year 2020 per our analysis of general ledger expense. Also, it should be noted that the PARs for COO notate higher percentage of time spent working at Head Start/Early Head Start than expensed to the general ledger. (Appendix V-Q – M Gill Salary Summary) Earnings record reports for Manvir Gill are provided for 2017 to 2020 (Appendix V-V) as requested. |

Corrective Action Goal #2 – Action 10 |

|

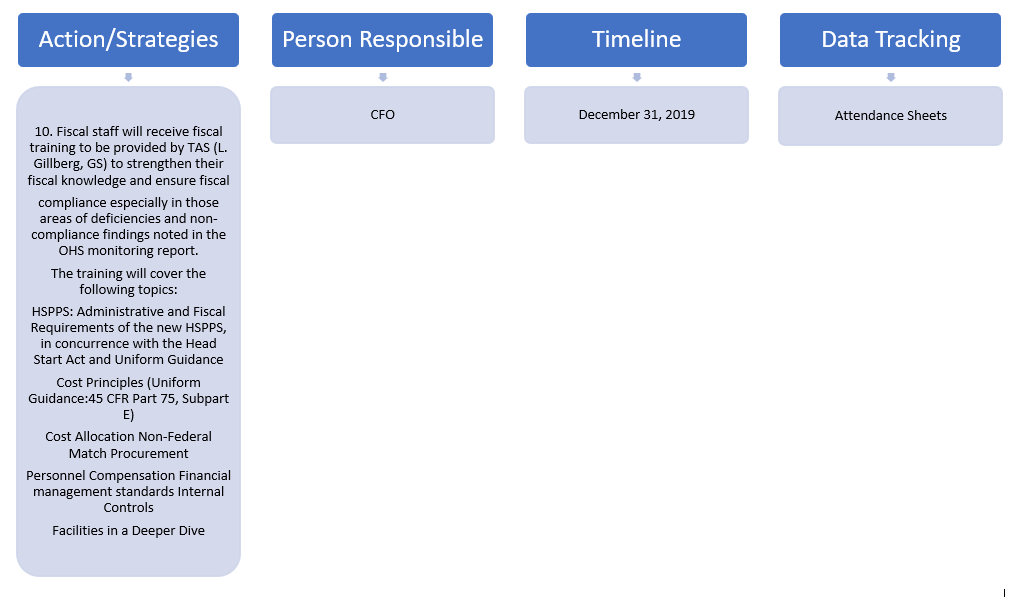

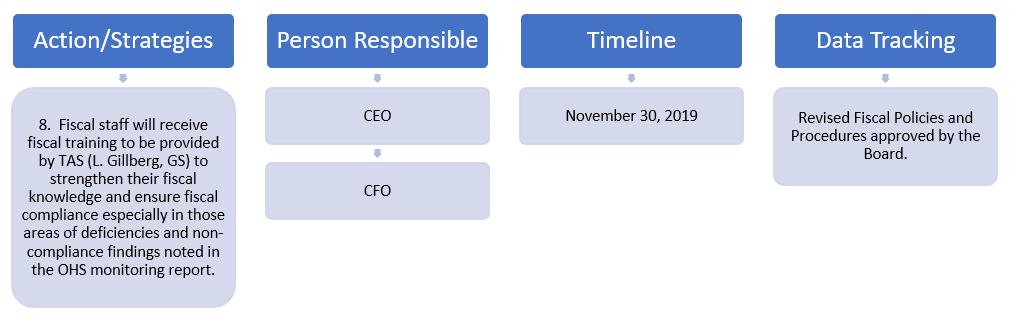

Fiscal staff will receive fiscal training to be provided by TAS (L. Gillberg, GS) to strengthen their fiscal knowledge and ensure fiscal compliance, especially in those areas of deficiencies and non-compliance findings noted in the OHS monitoring report. The training will cover the following topics:

Click here to view the agenda and sign-in sheets for Fiscal Training held on 11/20/2019 & 11/21/2019 |

Corrective Action Goal #3 – Action 1 |

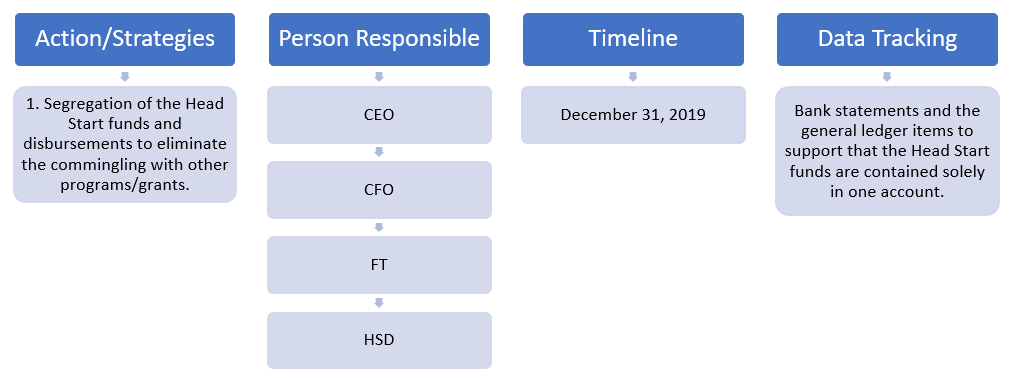

| Segregation of the Head Start funds and disbursements to eliminate the commingling with other programs/grants. |

Corrective Action Goal #3 – Action 2 |

|

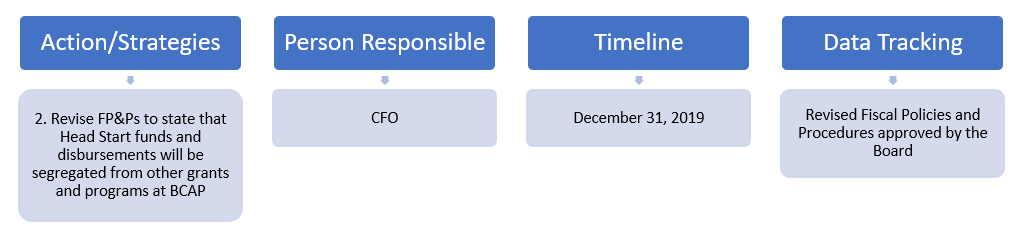

Revise FP&Ps to state that Head Start funds and disbursements will be segregated from other grants and programs at BCAP. |

Corrective Action Goal #3 – Action 3 |

|

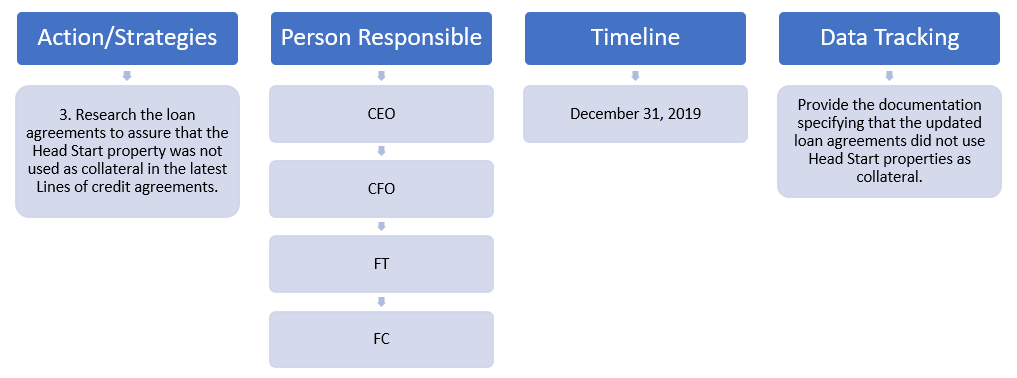

Research the loan agreements to assure that the Head Start property was not used as collateral in the latest Lines of credit agreements. Please click here to refer to Appendix V-X. Click here to view confirmation letter to Office of Head Start – Region II |

Corrective Action Goal #3 – Action 4 |

|

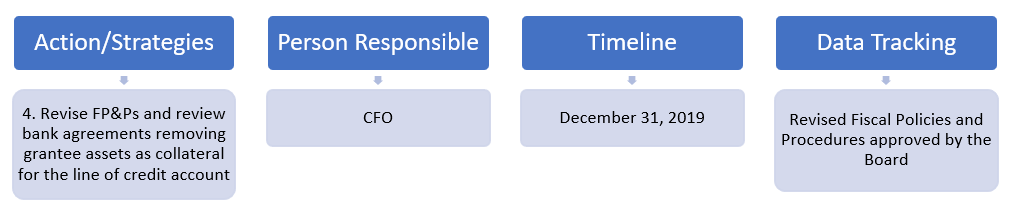

Revise FP&Ps and review bank agreements removing grantee assets as collateral for the line of credit account. |

Corrective Action Goal #3 – Action 5 |

| Establish Personal Activity Reports (PAR) for administrative staff that will support the allocations of salaries and benefits and will ensure compensation for personal services satisfy the standards of documentation of personnel expenses. |

Corrective Action Goal #3 – Action 6 |

|

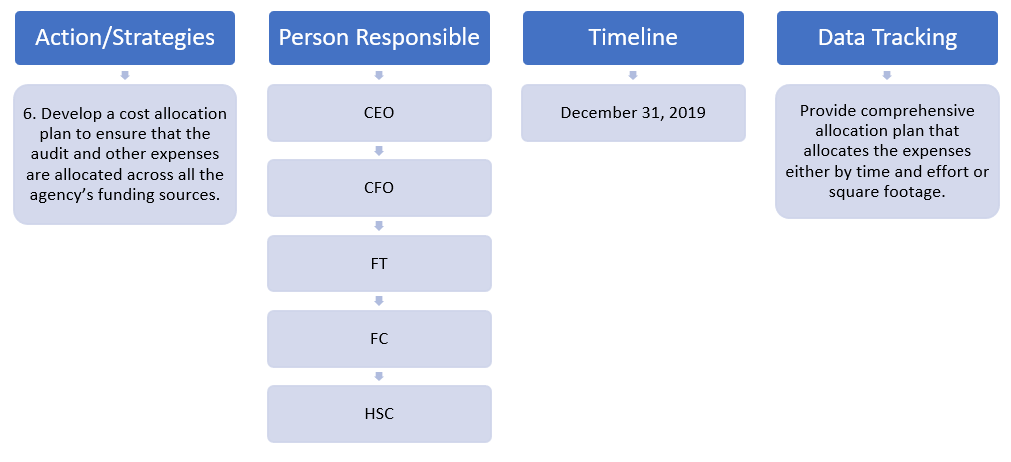

Develop a cost allocation plan to ensure that the audit and other expenses are allocated across all the agency’s funding sources. |

Corrective Action Goal #3 – Action 7 |

|

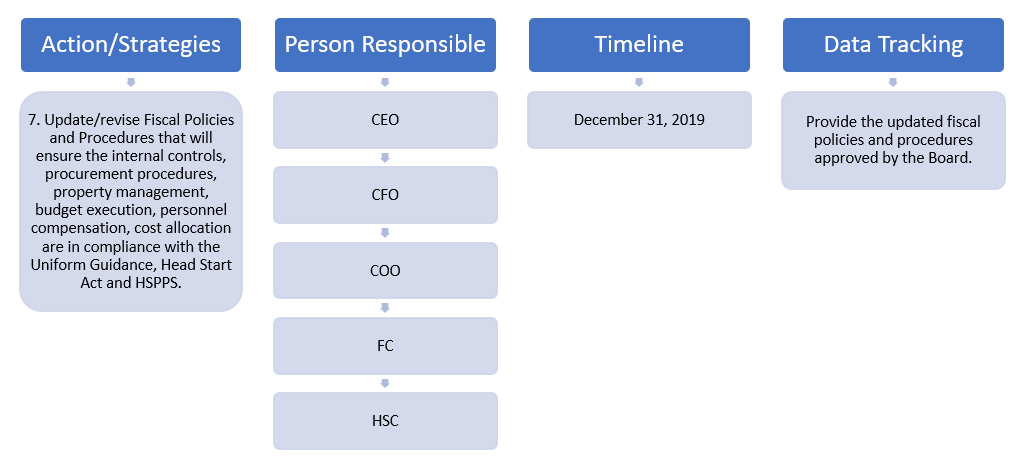

Update/revise Fiscal Policies and Procedures that will ensure the internal controls, procurement procedures, property management, budget execution, personnel compensation, cost allocation are in compliance with the Uniform Guidance, Head Start Act, and HSPPS. |

Corrective Action Goal #3 – Action 8 |

|

Fiscal Staff will receive fiscal training to be provided by TAS (L. Gillberg, GS) to strengthen their fiscal knowledge and ensure fiscal compliance, especially in those areas of deficiencies and non-compliance findings noted in the OHS monitoring report. |

Corrective Action Goal #3 – Action 9 |

|

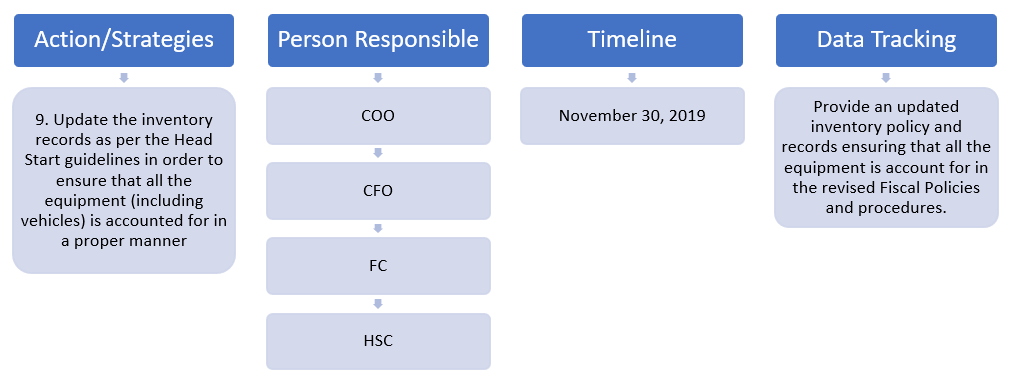

Update the inventory records as per the Head Start guidelines in order to ensure that all the equipment (including vehicles) is accounted for in a proper manner. |

| Attachments provided in response to Office of Head Start, Region II letter dated 8/24/2020: Item # 4 – NOAs for period 2017-2020 (Appendix VI – A – 2017 NOA, Appendix VI – B – 2018 NOA, Appendix VI – C – 2019 NOA, Appendix VI – D – 2020 NOA) Item # 5 – Audit reports for fiscal years ended 2017-2019 (Appendix VI-E Audit FY2017, Appendix VI-F Audit FY2018, Appendix VI-G Audit FY2019) Item # 6 – Final SF-425 reports for award periods 2017-2020 with reconciliation to the original and revised reports and general ledger reconciled to each SF-425. This item has been referred to our auditors for their input and review prior to submission. Item # 7 Cost Allocation Plan (Appendix III – Cost Allocation Plan) and prior year plan (Appendix VI-H – Cost Allocation Plan-2019 & Prior) |